Chapter 22 — Fiscal Policy

Cambridge International AS & A Level Economics (9708) · Unit 5.2 · 4th edition coursebook

Learning objectives

- Define the meaning of fiscal policy.

- Define the meaning of a government's budget.

- Explain the difference between a government budget deficit and a government budget surplus.

- Explain the meaning and significance of the national debt.

- Explain the difference between indirect and direct taxes.

- Explain the difference between progressive, regressive and proportional taxes.

- Explain rates of tax: marginal and average rates of taxation (mrt, art).

- Analyse the reasons for taxation.

- Explain the difference between current and capital government spending.

- Analyse the reasons for government spending.

- Explain the difference between expansionary and contractionary fiscal policy.

- Discuss, using AD/AS analysis, the impact of expansionary and contractionary fiscal policy on equilibrium level of national income, the level of real output, the price level and employment.

Key terms

- fiscal policy

- The use of taxation and government spending to influence aggregate demand.

- budget

- An annual statement in which the government outlines plans for its spending and tax revenue.

- budget surplus

- Government revenue exceeding government expenditure.

- budget deficit

- Government expenditure exceeding government revenue.

- balanced budget

- Government revenue equalling government expenditure.

- automatic stabilisers

- Changes in government spending and taxation that occur to reduce fluctuations in aggregate demand without any alteration in government policy.

- cyclical budget deficit

- A budget deficit caused by a decline in economic activity.

- structural budget deficit

- A budget deficit caused by an imbalance between government spending and taxation.

- tax base

- The coverage of what is taxed.

- national debt

- The total amount of government debt.

- specific taxes

- Taxes that are charged as a set amount per unit.

- sin taxes

- Taxes on products considered harmful to consumers.

- direct taxes

- Taxes on income and wealth.

- tax avoidance

- The legal bending of the rules of the tax system to pay less tax.

- tax evasion

- The illegal non-payment or underpayment of a tax.

- regressive tax

- A tax which takes a larger percentage of the income or wealth of those on low incomes.

- proportional tax

- A tax which takes the same percentage of the income or wealth of all income groups.

- marginal rate of taxation (mrt)

- The proportion of extra income taken in tax.

- average rate of taxation (art)

- The proportion of income that is taxed.

- current government spending

- Government spending on providing goods and services.

- capital government spending

- Government spending on investment.

- exhaustive government spending

- Government spending which makes use of resources.

- non-exhaustive government spending

- Government spending which allows others to decide how resources are used.

- expansionary fiscal policy

- Increases in government spending and cuts in taxes designed to increase aggregate demand.

- contractionary fiscal policy

- Decreases in government spending and increases in taxes designed to reduce the growth of aggregate demand.

- discretionary fiscal policy

- Deliberate changes in government spending and taxation.

22.1Fiscal policy and the budget

Fiscal policy is the use of taxation and government spending to manage aggregate demand in order to achieve the government's macroeconomic aims. The government's annual budget is a statement of its fiscal policy. The budget often receives close media attention because it serves both as a statement of policy intentions and as an indicator of economic performance. In the budget statement, the finance minister outlines the government's spending and taxation plans for the year ahead.

A budget surplus arises when tax revenue exceeds government spending. A budget deficit occurs when government spending exceeds tax revenue. A balanced budget is achieved when the two are equal.

Most governments aim for a balanced budget over time. In the short term, however, a government may aim for, or welcome, a budget deficit if the economy is operating at a low level of activity. Such a deficit may arise both from deliberate government action and from automatic stabilisers. If economic growth slows and unemployment rises, a government may cut tax rates and increase its spending. At the same time, even without any policy change, spending on unemployment benefits rises and tax revenue falls automatically as the slowdown reduces incomes and profits.

Cyclical and structural deficits

A deficit caused by a fall in economic activity is known as a cyclical budget deficit. Governments are typically not very concerned about a cyclical deficit, because it will tend to disappear of its own accord as economic activity recovers. A structural budget deficit, in contrast, arises when the government is committed to too much spending relative to its tax revenue. A structural deficit does not vanish when GDP increases. In practice, an actual budget deficit may contain both cyclical and structural elements.

Figure 22.2 shows the difference between the two. Line XX represents a situation in which, at the full-employment level of real GDP, there is no deficit at all — the budget is structurally balanced. Line ZZ, however, shows a deficit that persists even at full employment. At an income level below full employment, the deficit on ZZ can be split into a cyclical portion (which will close as the economy recovers) and a structural portion (which will not).

A deficit will decline, at least in the short run, if tax revenue rises or government expenditure falls. Yet it is also possible that a rise in spending or a cut in tax rates or the tax base could in time reduce the deficit. This is because such measures could stimulate economic activity. For example, if increased spending on training raises workers' skills, they may earn higher wages and so pay more tax in future.

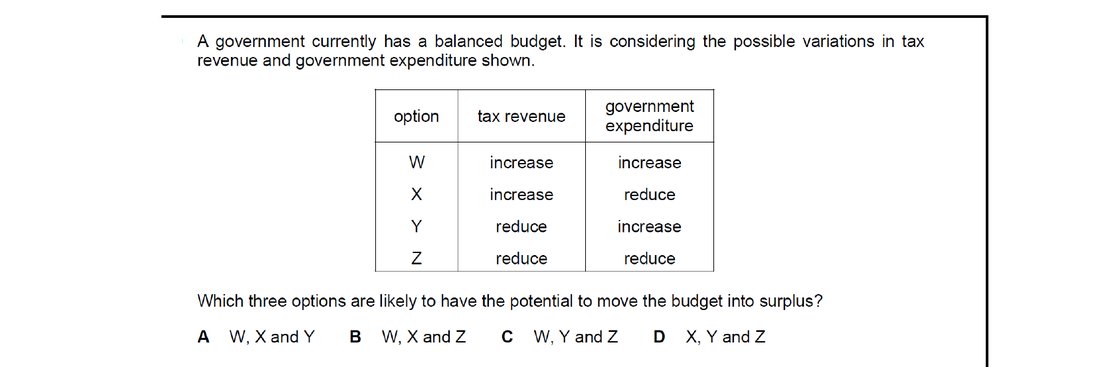

A surplus is created when tax revenue rises relative to expenditure. So any combination is potentially surplus-creating except the one where revenue falls and expenditure rises (Y). The three remaining options — W (both rise, revenue must rise by more), X (revenue rises and expenditure falls — unambiguously a surplus) and Z (both fall, expenditure must fall by more) — all have the potential to deliver a surplus.

22.2The national debt

The national debt is the total amount of government debt — the accumulated stock of what a central government, or the whole public sector, has borrowed over time. It is often expressed as a percentage of GDP. The national debt is connected to budget deficits and surpluses: a deficit in any given year adds to the debt, while the extra revenue earned from a surplus can be used to pay down part of the debt.

The national debt tends to increase during economic downturns, because in such periods government expenditure rises more quickly than tax revenue. A government may also spend more than it raises even during economic booms — a structural deficit — which adds to the debt in good times as well as bad. Military conflicts can result in significant increases to the national debt as well.

Disadvantages of a large and growing national debt

There is an opportunity cost in the interest payments required to service the debt: the revenue used for interest could have financed other public spending, such as the building of new hospitals. A large national debt may make financial institutions, firms, individuals and foreign governments reluctant to lend to the country in future, because they may doubt the government's ability to pay the interest and repay the sums borrowed. Heavy borrowing may also push up the rate of interest the government has to offer.

National debt and external debt

National debt is not the same as external debt. Some of a country's national debt is owed to its own citizens — for example, households who have bought government saving certificates and domestic banks that have bought government bonds. Interest paid on this domestically held portion stays inside the country. Payments to foreign lenders, by contrast, involve an outflow of money from the country.

The national-debt-to-GDP ratio falls if some of the debt is repaid or if GDP rises faster than the debt — even an unchanged debt becomes a smaller share of a growing economy.

National debt is a stock variable: it is the total amount the government owes as a result of past borrowing that has not yet been repaid. So it equals the accumulated borrowing of the government over time. The difference between spending and tax revenue is the annual budget deficit (a flow), interest payments are the cost of servicing the debt, and household debt is a private-sector liability — none of these is the national debt.

22.3Taxation

Taxes can be grouped in a number of ways. One of the main divisions is between indirect taxes and direct taxes.

Indirect taxes

Indirect taxes are taxes on the sale of goods and services. They are called indirect because, although they are largely paid by consumers, they are collected by the firms that supply the products. It is the firms that are legally responsible for handing the tax to the government. Firms try to pass on as much of the tax as possible to consumers in the form of higher prices. The proportion they can pass on depends on the price elasticity of demand: the more inelastic the demand, the larger the share of the tax that ends up being borne by consumers.

The two most common indirect taxes are VAT (value added tax) and GST (general sales tax). Both are ad valorem taxes, charged as a percentage of the price of the product. There are also specific taxes, which have a set amount of tax per unit sold. Indirect taxes on particular products are sometimes known as excise duties. Some excise duties are referred to as sin taxes, imposed to discourage people from buying products that are harmful to their health.

Direct taxes

While indirect taxes are taxes on spending, direct taxes are taxes on income and wealth. Two important examples are income tax (a tax on the income of individuals, sometimes called personal income tax) and corporate tax (a tax on the profits of firms, also known as corporation tax or corporate income tax).

Indirect taxes versus direct taxes

In recent decades there has been a tendency for governments to rely more on indirect taxes. Indirect taxes can be changed relatively quickly and easily. They are cheaper to collect than direct taxes because firms do part of the administrative work. They can also be used to discourage the purchase of particular products.

The main advantage claimed for indirect taxes is that they do not discourage effort, innovation and saving. Higher direct taxes may put some people off joining the labour force, stop some workers from doing overtime, and lead others to cut the standard hours they work, because each hour of work yields less disposable income. Direct taxes may also act as a disincentive to save, because income can be taxed twice — once when it is earned and again when interest is received on any part that is saved. High direct taxes on firms may stop them introducing new methods and products if they expect their post-tax income to be too low.

These disincentive effects are not certain, however. Some workers may instead choose to work more hours to maintain their disposable income when direct taxes rise. High direct taxes may also encourage tax avoidance and tax evasion.

A greater reliance on indirect taxes can make the distribution of income less even, because indirect taxes are regressive: a fixed tax on a product takes a larger share of a low income than of a high one. Indirect taxes can also be inflationary, pushing up the price level. The imposition or increase of indirect taxes places an extra cost on suppliers, which can lead to higher prices and feed expectations of further price rises, contributing to cost-push inflation. High rates of indirect tax may also encourage people to try to avoid paying them, for example by smuggling goods into the country to evade import tariffs.

Progressive, regressive and proportional taxes

While indirect taxes are regressive, direct taxes are usually progressive. A progressive tax is one that takes a higher percentage of a person's or firm's income as that income rises. In a typical progressive income tax, low slices of income are taxed at low rates (or not at all), and higher slices are taxed at progressively higher rates. As a result, the share of total income paid in tax rises as income rises.

A regressive tax takes a smaller percentage of income as income rises, so it takes a higher percentage of the income of people on low incomes. A proportional tax is a fixed-percentage tax: the rate does not change as income changes. A 'pure' flat-rate system would apply a single rate to all forms of tax — income tax, corporate tax, and sales tax all at the same percentage. Such a system is simple to understand and administer but is regressive overall.

Marginal and average rates of taxation

The marginal rate of taxation (mrt) is the proportion of extra income taken in tax. If a person earns an additional unit of income and a fraction of that unit is paid in tax, that fraction is the marginal tax rate. The average rate of taxation (art) is the proportion of a person's total income that is taken in tax.

In the case of a progressive tax, the marginal rate is higher than the average rate, because each extra slice of income is taxed at a higher rate than the slices below it. In a regressive tax, the marginal rate is lower than the average rate. In a proportional tax, the marginal rate equals the average rate.

The reasons for taxation

Taxes are imposed for several reasons. One is to raise revenue to finance government spending on merit goods such as education and public goods such as defence. A government also uses taxation to influence aggregate demand: it raises tax rates or widens the tax base when it wants to reduce AD, and does the reverse when it wants to support AD. Influencing aggregate demand is probably the main reason taxes are imposed; in theory a government could finance its spending simply by printing money, but doing so would be highly inflationary. Taxation reduces private sector demand and so frees up resources for use by the public sector.

A progressive income tax may be used to distribute income more evenly. By taking a higher proportion of high incomes than of low incomes, it narrows the gap between the disposable incomes of rich and poor households. The gap can be further narrowed if some of the tax revenue is used to provide cash benefits to those on low incomes.

Taxes are also used to discourage the consumption of certain products. These may be imports, where a government is concerned that spending on imports is exceeding earnings from exports. They may also be demerit goods, where taxation is intended to improve people's health and the environment.

22.4Government spending

Government spending can be divided into three categories: spending on transfer payments (which is not counted in measures of national income), current spending and capital spending.

Transfer payments are welfare payments to certain groups of people. They include spending on unemployment benefits, state pensions and interest payments on the national debt. Current government spending is spending on goods and services used to provide state-financed services. It covers operating costs such as the wages of teachers in state schools and the medicines used in state hospitals. Capital government spending is spending on capital goods used in the public sector, such as building state schools and hospitals.

Government spending can also be divided into exhaustive and non-exhaustive spending. Exhaustive government spending covers current and capital spending: it uses resources directly and is counted in aggregate demand and GDP. Non-exhaustive government spending is spending on transfer payments. It does not involve the government itself deciding how resources are used; rather, the people who receive the payments decide how to use the resources.

Reasons for government spending

The reasons for government spending are linked to the reasons for taxation. Governments spend to influence aggregate demand and thereby the level of economic activity. If private sector spending is thought to be too low, a government may inject more spending into the economy, aiming for a budget deficit by spending more than it raises in tax.

Government spending can also be used to increase aggregate supply. Spending on education, healthcare and infrastructure raises an economy's productive potential by improving the quality and quantity of its resources.

Spending on transfer payments is designed to ensure that people have a basic level of income, and so to avoid poverty and reduce income inequality. Unemployment benefits, for example, provide an income for those who have lost their jobs and would otherwise be at risk of falling into poverty.

Governments spend on merit and public goods to overcome market failure. As GDP rises, there is likely to be pressure on the government to spend more on these goods, as people develop higher expectations of, for example, the quality of education they receive. Advances in technology can also raise spending on healthcare, by making possible more complex operations that also require more expensive aftercare.

In practice, governments may also spend to win political popularity so that they can stay in power; spending in some countries rises noticeably just before an election. Pressure groups may also influence governments to spend more on particular causes, such as the environment. In assessing the likely effects of a change in spending, it is useful to consider not just the size of the change but also which items of spending are being altered.

Education spending shifts AD right because the spending itself is a component of government expenditure (G), and the construction of new schools — buildings, classrooms, equipment — represents real government spending injected into the economy. Higher AS and a more skilled workforce are long-run supply-side effects, not AD shifts; raising taxes would actually reduce AD. So the AD-rightward shift comes from the act of building more schools.

22.5Expansionary and contractionary fiscal policy

Expansionary fiscal policy is designed to increase aggregate demand. A government may increase its spending, cut tax rates, narrow the tax base in a way that lowers revenue, or some combination of these. It may deliberately increase an existing budget deficit so as to make a larger net injection into the circular flow of income.

Contractionary fiscal policy is intended to lower the growth of aggregate demand. The government reduces its spending, raises taxes, or both, and may aim for a budget surplus.

Changes in spending and taxation can result from changes in policy or from changes in economic activity. Deliberate changes are referred to as discretionary fiscal policy.

Automatic stabilisers

A government can also allow automatic stabilisers to influence aggregate demand. Automatic stabilisers are forms of government spending and taxation that change, without any deliberate government action, to offset fluctuations in GDP. During a recession, spending on unemployment benefits automatically rises because more people are unemployed, while tax revenue from corporate tax, income tax and indirect taxes falls as profits, incomes and expenditure decline. As GDP recovers, government spending on benefits falls and tax revenue rises again, dampening the swings in aggregate demand without any change in policy.

The impact of expansionary and contractionary fiscal policy on the macroeconomy

Governments may use contractionary fiscal policy tools to reduce demand-pull inflation. Income tax rates may be raised, the threshold at which people start paying the tax may be lowered, and the tax base may be widened. Governments may also cut their own spending; this may be the more favoured option in countries where only a small proportion of the population pays income tax. Higher taxes and lower government spending may reduce aggregate demand, or at least the growth of aggregate demand.

However, raising income tax to reduce demand-pull inflation may not work as planned. Workers may seek higher wages to maintain their disposable income, and if their wage claims are granted, firms' costs of production rise and this can generate cost-push inflation. Higher income tax rates may also create disincentive effects: some workers may respond to a reduction in disposable income by leaving the labour force, and others may emigrate to countries with lower tax rates. This reduces the economy's productive capacity and so reduces aggregate supply.

Expansionary fiscal policy may be used to increase a country's output and raise employment. If a country has high cyclical unemployment, the government is likely to try to increase aggregate demand. It might cut direct and indirect tax rates to stimulate higher consumer expenditure and investment, and add to aggregate demand directly by increasing its own spending. On an AD/AS diagram, the AD curve shifts to the right, raising the price level and lifting real GDP from its initial level to a higher level (see Figure 22.10).

The success of expansionary fiscal policy in stimulating economic growth and reducing unemployment depends on a number of factors. It may not be very effective if households and firms are worried about the future, because they may then save most of any extra disposable income they receive as a result of lower taxes and higher government spending. There is also the risk that the government may inject too much spending into the economy, causing demand-pull inflation. In deciding whether a government is using expansionary or contractionary fiscal policy, it is the intended effect on AD that matters.

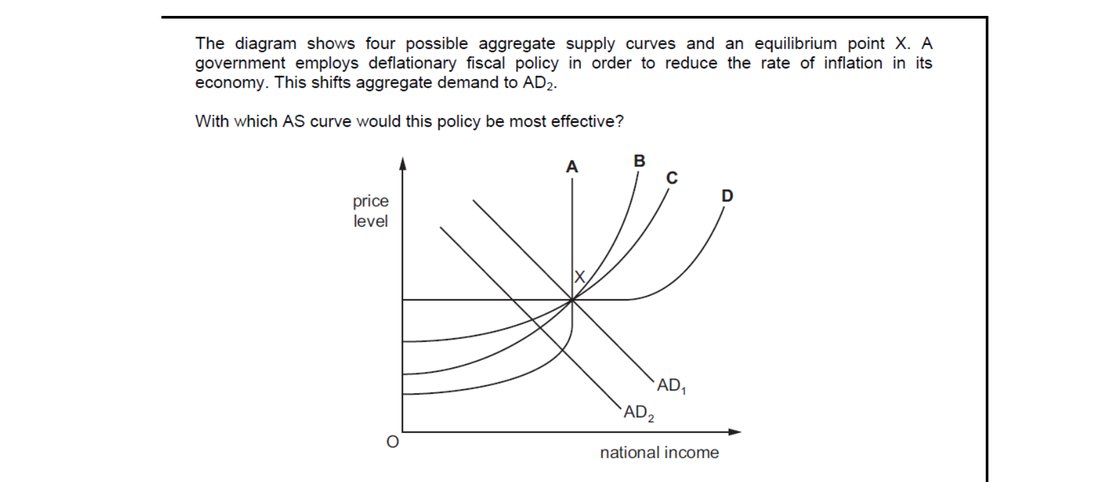

Deflationary fiscal policy is most effective at reducing inflation when the AS curve is relatively elastic at the existing output level, because a leftward AD shift then produces a large fall in the price level for a small fall in output. The flattest (most horizontal) AS curve — curve A — delivers the biggest price-level reduction for the AD shift, making it the AS curve under which the policy works best.

A budget deficit is expansionary — government spending exceeds tax revenue, injecting demand into the economy. Reducing the deficit therefore tightens fiscal policy, lowers aggregate demand and so eases demand-pull inflation. Cutting direct taxes would raise disposable income and AD; a lower exchange rate raises import prices; and a lower interest rate stimulates spending — all of which would tend to add to inflation.

End-of-chapter practice

Past-paper questions from CIE 9708. Pick A, B, C or D. Answers are saved on this device — press Download report (PDF) at the top to save them.

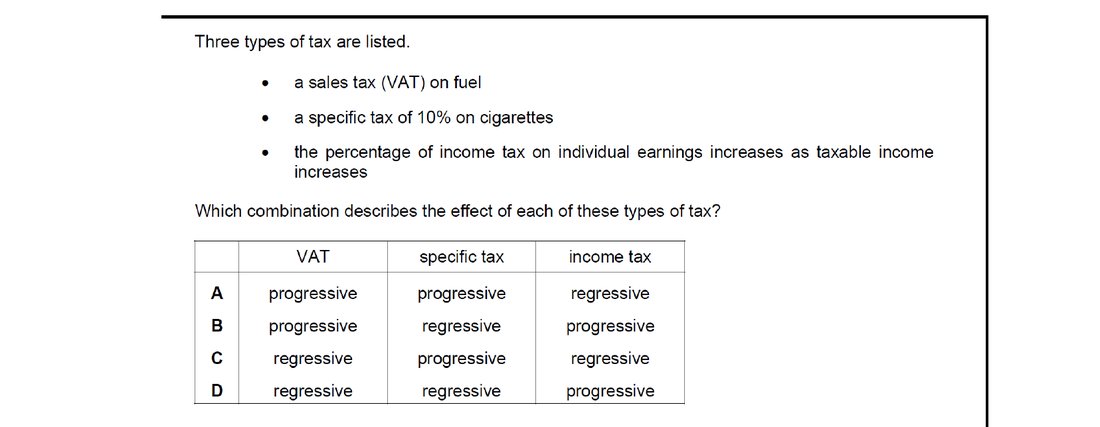

Sales tax on fuel and a specific tax on cigarettes are indirect taxes paid as a fixed share or flat amount per unit: they take a larger proportion of a poor person's income than a rich person's, so both are regressive. An income tax whose rate rises as taxable income rises takes a larger share of high incomes — by definition progressive. The pattern is therefore regressive, regressive, progressive.

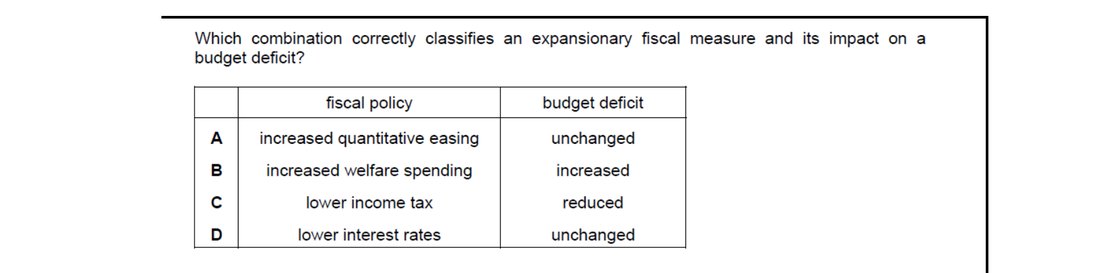

Expansionary fiscal policy means higher government spending or lower taxes. Quantitative easing and lower interest rates are monetary tools, not fiscal, so A and D fail. Lower income tax is fiscal but reduces revenue, so the deficit rises (not falls), so C is wrong. Increased welfare spending raises government expenditure — expansionary — and pushes the budget deficit upward, which is exactly what option B states.

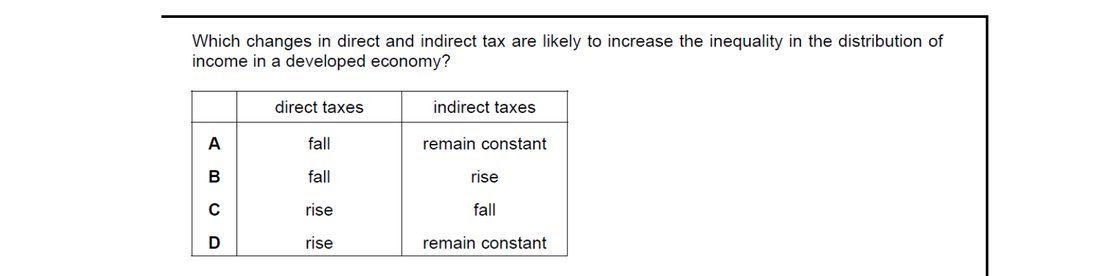

Direct taxes (e.g. income tax) are typically progressive — they take a larger proportion of high incomes — so cutting them benefits higher earners more. Indirect taxes (e.g. VAT) are regressive — they take a larger share of low incomes — so raising them hurts lower earners more. Falling direct tax combined with rising indirect tax therefore widens the post-tax income gap and increases inequality.

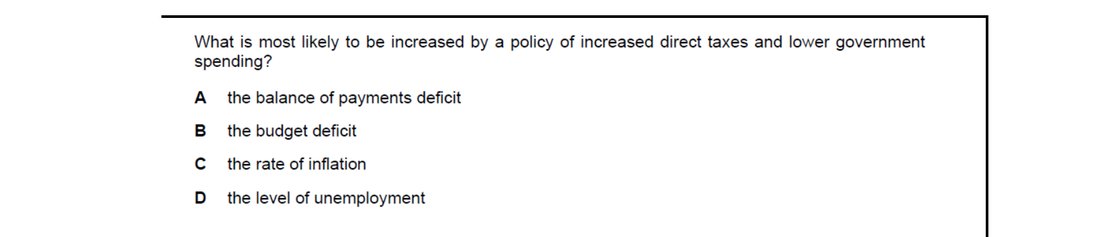

Raising direct taxes and cutting government spending is contractionary fiscal policy: disposable income falls and a major component of AD (G) is reduced, so AD falls. Lower AD causes firms to cut output and lay workers off, raising cyclical unemployment. The same policy mix would reduce — not raise — the budget deficit and inflation, and tends to improve, not worsen, the current account.

A regressive tax takes a higher proportion of income from low-income earners than from high-income earners — that is its defining feature. The marginal rate exceeding the average is true of a progressive tax (B), high collection cost is irrelevant to incidence (C), and a higher marginal rate at high incomes (D) describes a progressive tax. Only A captures the regressive structure.

Attempt the practice questions above to build your score.

Self-evaluation checklist

After studying this chapter, you should be able to:

- Understand that fiscal policy is the use of taxation and government spending to manage aggregate demand (AD) in order to achieve the government's macroeconomic objectives.

- Understand that the government's annual budget is a statement of its fiscal policy.

- Explain that a budget deficit arises when government spending is greater than tax revenue and a budget surplus arises when tax revenue exceeds government spending.

- Understand that the national debt is total government debt built up over time.

- Explain that indirect taxes are taxes on the sale of goods and services whereas direct taxes are taxes on income and wealth.

- Explain that indirect taxes are regressive and direct taxes are progressive.

- Understand that a proportional tax is a fixed percentage tax.

- Explain the reasons for imposing taxes.

- Explain that government spending can be divided into spending on transfer payments, current spending and capital spending.

- Analyse the reasons for the different types of government spending: transfer payments, current spending, capital spending.

- Differentiate between expansionary fiscal policy that seeks to increase AD and contractionary fiscal policy that seeks to reduce AD.

- Use AD/AS analysis to consider the impact of expansionary and contractionary fiscal policy on national income, real output, the price level and employment.

Want more practice? Drill this chapter's past-paper MCQs (104 questions) →